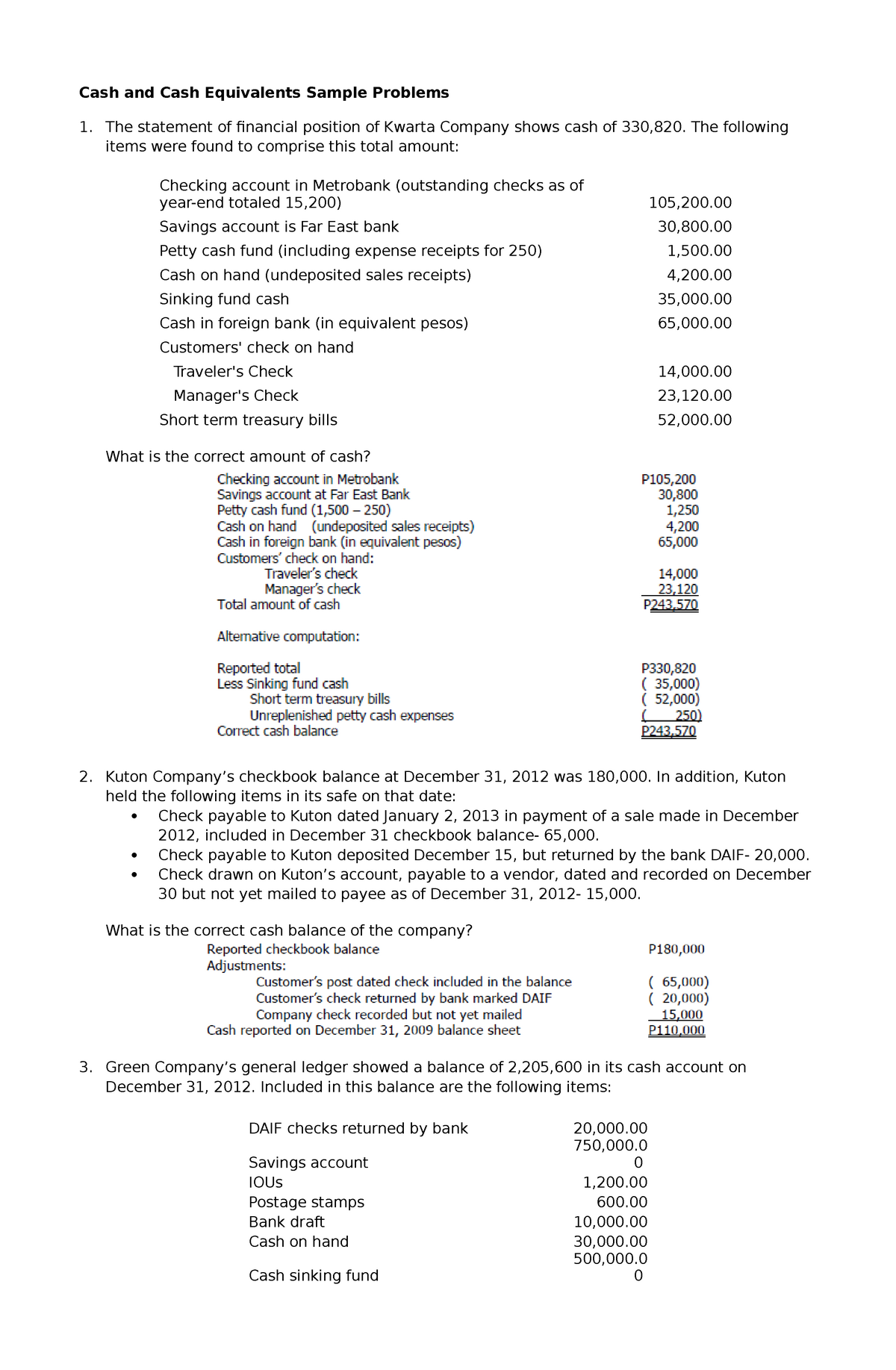

In order to do one to, new Smiths could have needed to borrow the money compliment of a household security mortgage, proper? Bankrate states you to in the 2012, 6.5% try a reasonable interest having a property collateral financing. Having fun with that rate of interest for example, a comparable mortgage amortization might have lead to an excellent $fifty,000 financing costing $8,698 within the focus. In order to a lender, believe it or not.

Whenever they paid back a total of $58,698, however their $50,100000 expanded to help you $80,525, they still netted $21,827, that’s more than $19,five hundred more than once they took the brand new Tsp loan

Yet not, the new Smiths would continue to have come better off regarding the next condition. There are also two observations:

- Making productive responsibility. A tsp financing, as with any mortgage up against an exact contribution retirement system, is only offered while you’re nevertheless working. For individuals who independent or retire, you ought to repay the mortgage completely. If you don’t the latest Internal revenue service deems the an excellent loan balance as the a taxable delivery.

- Tax cures. Teaspoon mortgage repayments are manufactured with immediately after-income tax bucks. This differs from Tsp contributions, which are pre-taxation. This is because effortless: a teaspoon loan isnt taxed (unless of course it gets a taxable delivery), so the cost is produced with after-tax dollars. On the other hand, appeal on the a house equity financing (to $a hundred,100000 equilibrium) get located well-known income tax cures, especially if you itemize their write-offs into Schedule A beneficial of tax return.

- Portfolio house allowance. This is actually the primary impression into Smith’s financing. Ahead of the financing, the newest Smiths had a hundred% of its Tsp purchased its L2040 finance.

Afterwards, it basically reduced their L2040 funding by the $fifty,one hundred thousand mortgage, upcoming secured themselves into G-fund’s rates out-of get back. Put simply, its house allowance appeared kind of like which:

Unless of course this new Smiths got meant for their house allotment to appear in that way, getting a tsp financing drastically changed their capital coverage. The latest truest chance of a tsp loan so is this:Delivering a teaspoon mortgage is substantially alter your financial support image. Unless you make up brand new impact away from locking inside G-funds output on your financing equilibrium, you chance undertaking a profile that is out-of sync that have forget the strategy.With that said, why don’t we check out the second cause individuals do take a tsp financing.

To possess purposes of this article, we’re going to skip plenty of talk from the investment opinions, risk https://cashadvancecompass.com/loans/emergency-payday-loan/, etcetera. We are going to focus on the use of Tsp given that an effective tax-deferred offers vehicles. This is what I found:

We are going to compare which to a few commonly recognized uses off Tsp mortgage proceeds (commonly defined as are exactly what appears towards very first step 3 profiles off Serp’s to possess expenses Teaspoon loan’)

Having fun with a tsp Mortgage purchasing a rental Property (Larger Pouches). Oh man. We could go-down a rabbit gap here. Yet not, let’s say that you will be a first and initial time local rental owner. Ahead of i determine whether a tsp financing is sensible, you will need to can even make yes the acquisition makes sense. After all, if you’re not prepared to end up being a property manager, then it does not matter where money originates from.

Let’s assume you manage the fresh new amounts & work with the case from the most of the a residential property landlording mentors one to you understand. All of them agree: it buy is an excellent financial support. If that’s the case, a bank would probably getting happy to fund the purchase. At all, a tremendous amount means that the brand new local rental earnings tend to be more than sufficient to make up for all hiccups that come in the process. Assuming a bank thinks it is really worth investment, next why must you use your own currency to finance new package to start with? One of the benefits from a property spending ‘s the suitable usage of leverage.